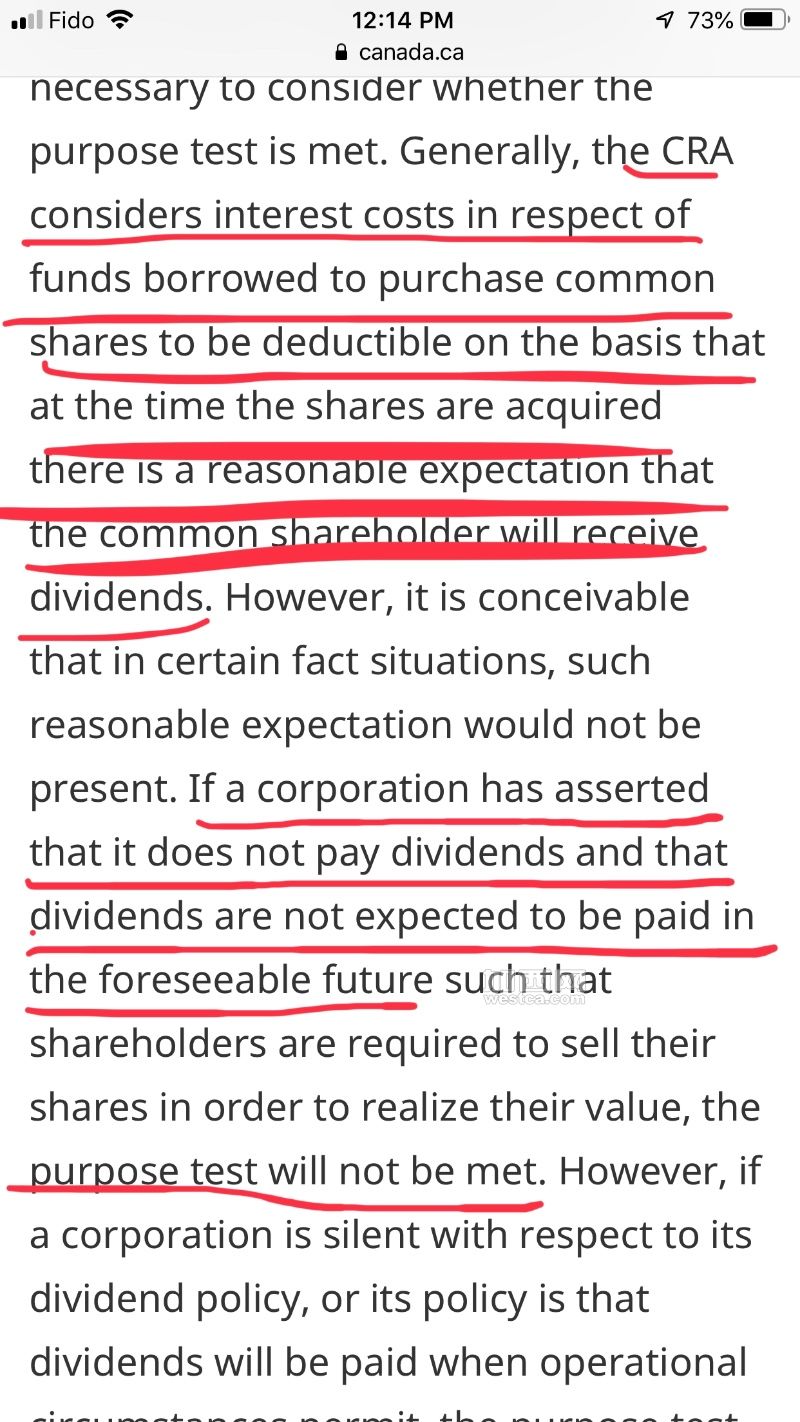

Where money is borrowed, the use of the money must be established and the purpose of that use must be to earn income. Borrowed money used to acquire a life insurance policy or property the income from which would be exempt will not qualify. The term use refers to the current use of the borrowed money and in certain situations may include indirect use. Where an amount is payable for property acquired, the property must have been acquired for the purpose of earning income (other than exempt income or to acquire an interest in certain life insurance policies).

It is important to note that capital gains are not considered to be income for tax purposes, so interest resulting from borrowing to generate capital gains alone will not be deductible. For example, interest on money borrowed to purchase a piece of art as an investment, would likely not be deductible.

Where money is borrowed, the use of the money must be established and the purpose of that use must be to earn income. Borrowed money used to acquire a life insurance policy or property the income from which would be exempt will not qualify. The term use refers to the current use of the borrowed money and in certain situations may include indirect use. Where an amount is payable for property acquired, the property must have been acquired for the purpose of earning income (other than exempt income or to acquire an interest in certain life insurance policies).

You cannot post new topics in this forum You cannot reply to topics in this forum You cannot edit your posts in this forum You cannot delete your posts in this forum You cannot vote in polls in this forum You cannot attach files in this forum You can download files in this forum

Global Announcement:

Global Announcement:

:

:

Jump to:

Jump to: